So, where is the real estate market headed in 2023?

Here’s a simple hack for you to predict what will happen this year, and any other year:

If you can forecast inflation, you can forecast interest rates, and then you can forecast REAL ESTATE!

Interest rates are not driven by the Bank of Canada or the Federal Reserve. They are driven by inflation. Full stop.

Let’s start our story by examining how the sudden drop in interest rates created inflation, and sent the real estate market into a tailspin.

What is inflation?

Too many dollars chasing too few goods.

During the COVID-19 pandemic, the Central Banks dropped rates to zero, but nothing happened to stimulate the economy.

So their next step was to print as much money as possible through “Quantitative Easing” (which means increasing the quantity of money circulating).

Next step was to send people “stimulus” money, so people started spending again. This is typically the beginning of inflation cycle. If governments start printing money, just know that it’s going to be a wild ride afterwards.

During Round 1 of stimulus, people saved the money because they were locked down.

(Also, when people are worried about the future, they tend to “sit” on their money).

Oops! Now the government needs to print more money. People still aren’t spending it, so people start paying down debt. The economy opens up and a LOT more people are rich, so they start buying everything they can!

Cars start selling for sticker price plus $10,000, and due to lockdown and lack of production, inventory levels of everything fall (or sell out) and the prices rise.

Inflation rises, and supply chain shortages continue (but don’t worry, it’s “transitory”).

Food, gas, and everything goes up 20-60%. The Government says it’s only 8%, and a bit of panic ensues.

In order to stop a mob of people descending on Parliament Hill or Washington because they can’t afford to eat, the Central Banks make if their number one priority to kill this crazy inflation… and UP go the interest rates.

On a side note… if you give people money that is essentially free, don’t be surprised if they all want to borrow, and buy goods or real estate at the same time, that ultimately bid up prices.

After the free money is gone, people have to pay higher carrying costs for loans and mortgages.

Remember, people buy the monthly payments, not price! When payments go up, people stop buying.

Here’s the crazy thing: 90% of the available dollars out there are in credit.

So, any increase in interest rates have a DRAMATIC effect on your monthly payment.

The next step… Central Banks say “Oops!” again.

They have printed too much money, things are nuts, and so begins the process of Quantitative Tightening and removing a quantity of money in the marketplace, so that people stop spending.

This has the effect of reducing demand, and reducing inflation.

Have I put you to sleep yet? No? OK! We will get to the future real estate market in a moment.

The “demand destruction” begins at this point.

When you raise rates, tighten money supply, and increase everyone’s payments on lines of credit, variable interest rate mortgages & car payment costs… people say “WTF!”

The rising rates stop people from spending and encourage people to save again because they can get a 4-5% return in a G.I.C or Treasury Bill, with no risk.

Real estate investors pull back because of lower yields, too.

Over the past 9 months, the real estate market has seen sales volume drop anywhere between 30-60%. Prices have declined anywhere from 12-40% across the country, depending on the type of dwelling and location. It’s mostly due to interest rates rising.

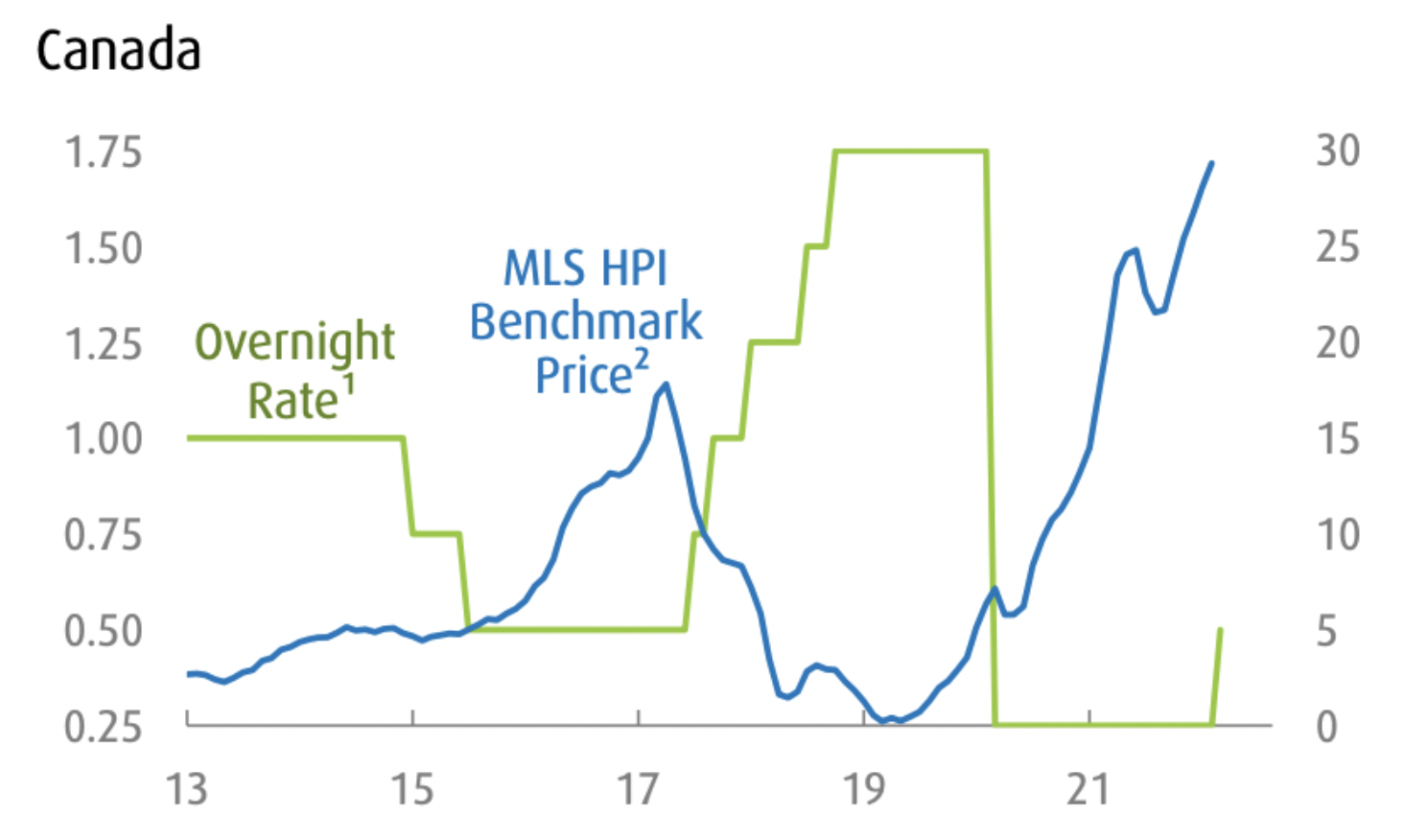

Look at the graph above, with data up to the early part of 2022.

It shows annual price growth in blue compared to interest rates. They’re almost perfectly inverse. When one goes up, the other goes down.

We all know what happened next… the green line spiked UP for the rest of 2022, and the blue line spiked DOWN.

Interest rates, more than anything else, are the most consistent predictor of real estate pricing.

What’s next for real estate?

Here is when we can begin to put it all together and start to predict the future of the real estate market.

Inflation is falling and will continue to fall. They use a 12-month trailing average, so as the high inflation months of February to May 2022 start to fall off, they will be replaced by the lower inflation rates of the next February to May 2023.

The overall rate will be much lower in the next few months. When you lower inflation, you can begin to “pause” the interest rate increase and eventually drop them again.

Many experts are forecasting that rates could be 0.75% to 1.5% lower by late June.

You might think that’s crazy because the Central Banks said inflation was “transitory” and “rates will be low for a long time”.

Then look at what happened!

If they got that wrong, why would we believe they will be right this time?

Inflation drops, interest rates drop, prices rise!

The formula is simple, and it’s been this way for a very long time.

The real estate market is right on schedule this year.

Traditionally, January is slow, followed by increasing demand (and a severe lack of inventory) and multiple offers from mid-February to after March break.

Too many Buyers chasing too little inventory, leading to multiple offers on the best properties.

After March Break, inventory levels typically begin to rise, and we will likely see a very busy Southern Ontario market from mid-April to mid-October.

It will be busy throughout the Summer, as people re-enter the market, now that they believe we have some stability in interest rates.

As of mid-March when we post this, here’s our best advice:

For buyers, you have about 8–10 weeks to buy a home before prices go up again.

Of course, our increasing Canadian population and our massive immigration numbers are like adding gasoline on the fire of this whole economic cycle.

If those experts we mentioned earlier are correct, and interest rates fall in June, pandemonium will return and prices will begin to rise.

For Sellers, you might benefit right now from lower inventory levels. You may also have a great window coming up soon. When rates drop, your value increases.

If you’re moving to a larger home, your perfect scenario is to buy/sell now with a May/June closing, and get the benefits of lower rates at today’s prices.

Remember the pattern…

Inflation determines interest rates!

Interest rates determine the demand for real estate!

Go forth with confidence knowing this information, and you’ll be able to forecast any real estate market.

Special thanks to our longtime friend & mentor Glenn McQueenie, for his wisdom and insights and providing the core theme of this post.